In recent years, many investment institutions have invested in some new robot companies. The market space in the industry itself is not very large, and the fragmentation is very serious. In the future, when the listing is difficult, the acquisition will become the future exit of these institutions from the invested companies. The important path. So is the acquisition really an important exit path for robotic investment institutions in the future? Which companies are more likely to be acquired? By analyzing the acquisitions of robots at home and abroad over the past few years, Io's think tanks have drawn some basic conclusions.

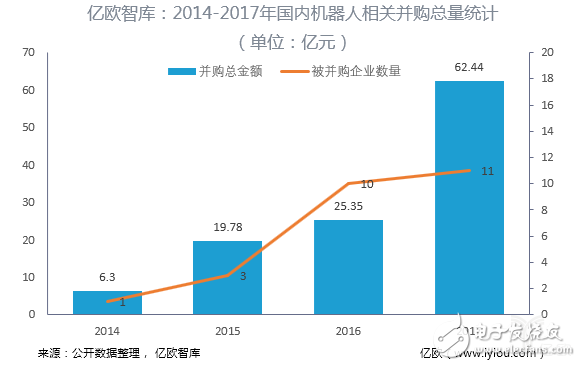

In terms of domestic robot-related acquisitions, according to the statistics of the billion euro think tank, the relevant mergers and acquisitions basically started from 2014. By the end of 2017, the acquisition of robot-related listed companies (acquisition of more than 50% of the shares) occurred in 25 cases from other companies or other listed companies to acquire industrial robot companies. The total investment is about 11.4 billion yuan. Among them, most of the acquisitions took place in 2016 and 2017, starting with 10 and 11 respectively. In terms of the number of acquisitions, since 2016, robot-related acquisitions have started to rise and continue to grow.

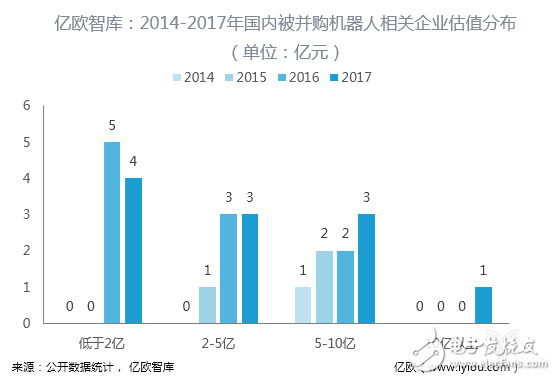

Although the number is quite large, the valuation of the acquired company is not high. The valuation of M&A before 2016 is generally low at several hundred million yuan. After that, although the valuation of the vast majority of acquired companies is still not higher than 1 billion yuan, the number of enterprises with 5-10 billion yuan has increased over time. Compared with many current startups in the B round of income, but hundreds of millions of dollars in valuation, many industrial robots have annual income of tens of millions, the valuation is only a few hundred million, the market sales rate PS is very low, which may be The lack of imagination in the industrial robot market has a lot to do with it. If this PS value is maintained, many companies in the current A round of financing may be listed in the future, and the secondary market valuation may be lower than the valuation of the primary market.

In terms of the purpose of the acquisition, although the announcement of the relevant acquisition will refer to the purpose, it is more ambiguous to describe it in terms of intelligent manufacturing. From the perspective of the business relevance of the acquired and acquired companies, Yiou has probably divided the relevant acquisition purposes: industry integrators to acquire robot ontology, robotic ontology acquisition integrators, product manufacturing enterprises, new incoming robots for industrial chain acquisition, robotic ontology acquisition upstream Parts companies and other purposes. According to statistics, among the 25 acquisitions, industry equipment manufacturers/integrators have acquired robotic ontology companies accounting for about 50%. Considering that there are fewer upstream core technology vendors in domestic robots, and with the increasing application of robots in various industries, it is highly probable that professional industry integrators will acquire robot manufacturers in the future.

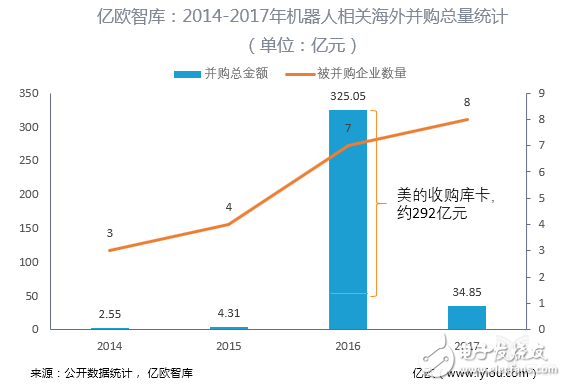

Domestic robots overseas acquisitions are also very active. In particular, in 2016, Midea acquired KUKA for nearly 30 billion yuan, which made the acquisition of robots reach its peak and became a landmark event in the industry. But not only the United States, the overall overseas acquisition of robots began in 2014, and the number showed a slow growth year by year, although The number of domestic acquisitions is slightly less (22), but the average amount is higher. (For the sake of comparison, this time the US dollar is used for RMB 6.5, and the exchange rate of the euro to RMB 7.8 is unified into RMB.)

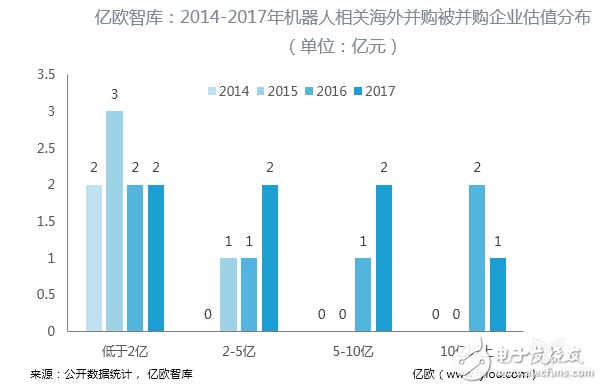

From the valuation of the acquired companies, the valuation of foreign-acquired companies is generally higher than domestic, and the average is about double the domestic level, especially for enterprises with valuations higher than 1 billion yuan. This may also be related to the nature of the business of foreign acquired companies. Many foreign acquired companies are engaged in core technologies such as motion control.

Based on the purpose of domestic related acquisitions, Io's think tanks have divided the relevant foreign acquisition purposes, and found that such acquisitions are mainly based on the acquisition of upstream core technologies (control and vision) and downstream integrated applications, which together account for about 73%. The core technology is 41% and the downstream integration is 32%. However, as some domestic powerful robot companies complete the layout, the reduction of optional targets and the increase in international trade friction, the overseas acquisition of Chinese companies may slow down.

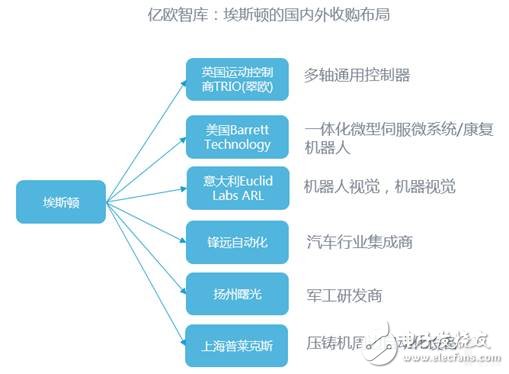

Through the acquisition analysis of related robots at home and abroad, Yiou think tank found that after the acquisition of the past two years, some powerful domestic robot companies, or manufacturing companies, have initially completed the layout from upstream core components to downstream industry integration ( For example, the above picture is Eston Automation), but there are still many robot-related companies that have only acquired some of these links, and have not completed the entire industry chain layout.

Considering the layout of the industrial chain, the early stage of the acquisition is more cost-effective, and the price of hundreds of millions of dollars can be completed in the hands of listed companies, and the process is relatively simple. Previous domestic acquisitions have a lower amount, and may have a lot to do with the acquired companies. In the future, with the development of the robot industry as a whole, the acquisition of robotics from the perspective of industrial chain layout will not become high, and the main driving force for the acquisition may become the scale of the company's income. The listed companies will use this to expand the market value, or unlisted companies Seeking a listing.

At present, domestic industrial robot investment mainly focuses on the robot body part, many institutions are also paying attention to the upstream core components, while the industry integrators with lower technology content have received less attention. The emerging robotic ontology manufacturers that have been invested in the past two years are mostly key technology-type manufacturers, which have advantages from the perspective of longer-term market competition. However, from the perspective of acquisition, the system integrator PS is lower, but it is easier to quickly expand business data. Is to seek a large-scale listing or increase market value, the acquisition of professional industry integrators, follow-up is a better choice.

In addition, key technologies such as robot vision are still relatively early, but a number of manufacturers with technology have also been born in China. With the deep application of robot vision in the future, these companies may be well-received in the future, provided that the valuation is not high.

Led Wall Display,Outdoor Advertising Sign Banner,Advertising Digital Signs Banner,Outdoor Signs Banner

APIO ELECTRONIC CO.,LTD , https://www.displayapio.com